Is venture really broken?

#34 | On gigafunds, cottages and bubbles

“Markets can remain irrational longer than you can remain solvent.” applies to the public markets. The private markets parallel could sound something like “your bet can stay contrarian longer than the company’s runway”.

The idea of contrarian investing is appealing, but a contrarian bet is good only when it is contrarian just for a short time. I think many in the early-stage investing community are missing this crucial piece.

If you are an early-stage investor today, your worst enemy is A16Z.

You look back at the good old days when venture was a cottage industry, when the grass was greener, funds smaller and DPIs bigger, and you wish you could just go back in time before the evil gigafunds ruined everything.

They are capital agglomerators, not venture investors: they are in this game for the 2%, not the 20%. Their (venture) arrogance is so big that they believe they can generate hundreds of billions in exits, while truth is they are using this narrative to get rich from management fees while destroying what used to be a beautiful artisanal craft - early-stage investing.

You hate to be publishing another piece that opens with their name in the first line, but no one was ever fired from talking about Andreessen Horowitz, so you have to reluctantly play the game.

Latest episode that gave early-stage investors material to put into their newsletter came from Martin Casado’s twitter, one of A16Z’s GPs, when he stated that “Follow on capital tends to be more and more consensus aligned.”

The problem, critics say, is the concentration of money in the hands of a few funds like his, so big that they shouldn’t be considered venture funds anymore, that have an irresistible gravitational pull towards their ideas and thus flatten the variety of topics that get funded.

Looking at the numbers, that show an unprecedented concentration of money in the hands of a few funds and companies, some of the critics have suggested we should separate the rounds done by the gigafunds from all the rest - remember, they are not venture funds anymore, so why shall we pollute our own numbers with theirs?

I believe this is a dangerous argument we are getting into.

It’s risky because saying “they’re not a venture fund” just kicks the can down the road without addressing the core of the issue: venture investing has changed at every stage, and if you look closely you can see the same dynamics happening also within the early-stage investors community, even in those deals that are not yet “polluted” by gigafunds’ arrogance.

The idea of “non-consensus investing” has always been appealing for VCs, and it makes a lot of theoretical sense: to capture the most out of a transaction you want to find deals that have the biggest delta between perceived value and real value.

The issue is in the word “perceived”.

Venture Capital is a weird industry, that needs to generate returns 10 years in the future, but that assesses quality looking at the past. There is no real way to define a Tier 1 fund, except by looking at what deals they’ve done in the past inferring their multiple at exit, or looking at who has invested in companies that are (now, in the present) perceived as winners.

It feels wrong, I know, but even the most die-hard haters of gigafunds can’t avoid celebrating big rounds of their portfolio companies at high valuations as if that was the end goal of building a company. Also these people need to raise next fund, have LPs they need to pitch to and need something to show.

Today’s world of venture is one of storytelling and hype, one of concentration and kingmakers. In this world, being contrarian is riskier than ever.

If you believe that this happens only when gigafunds are involved, you are very wrong.

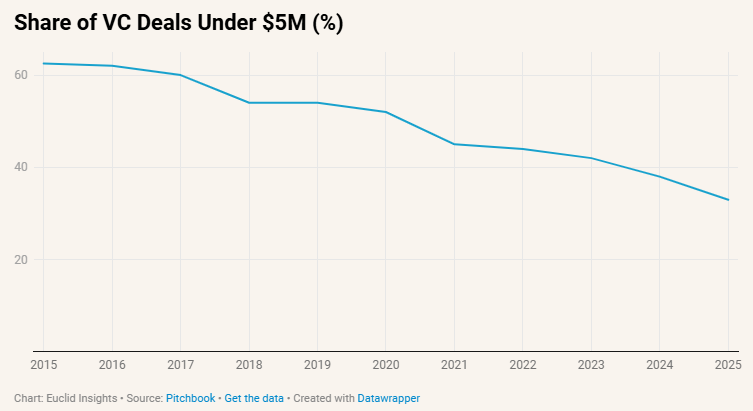

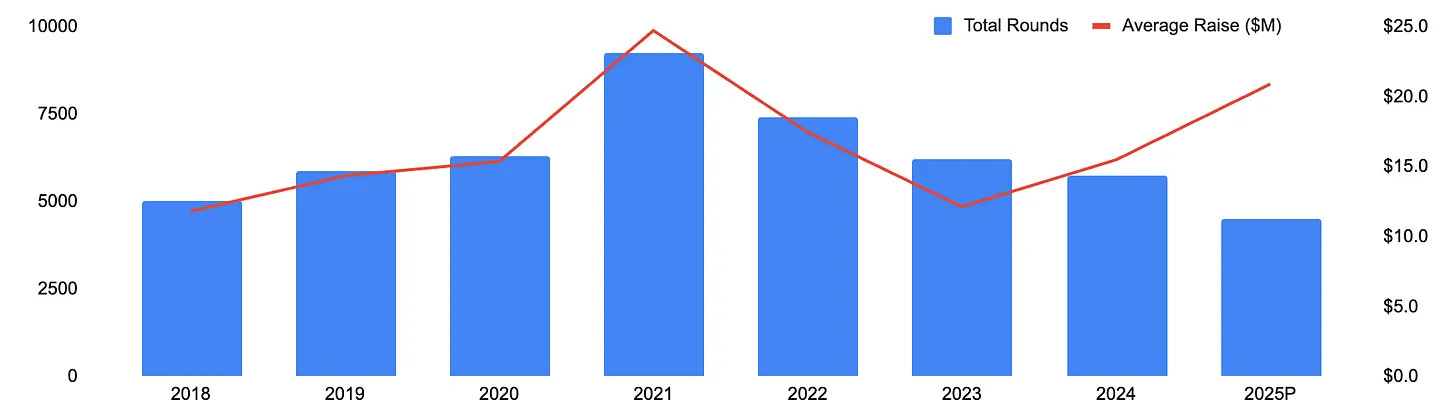

Rounds are getting bigger, at every stage, and are getting smaller in number. This means that, even if you play at the earliest stages, you can’t avoid to consider what your downstream funds like. That is true even if the downstream funds are not the gigafunds everybody hates.

This feels wrong, and I bet (even though I don’t have the data to back my bet) that this is not serving well the overall ecosystem. When only a few topics get funded, when a few kinds of founders get backed, we are implicitly capping the overall value we are creating for the society.

However, as wrong as this all feels, venture funds need to survive - need to be top of mind for founders and raise money from LPs.

It is proven that it’s not worth trying to time bubbles in public markets. Even if you think the markets are overvalued, you are usually better off riding the bubble until it bursts than getting out of the market and waiting they return to fair valuations. In a market that grows out of control, the opportunity cost of not riding it is very high.

I have a feeling we are living a similar moment in private markets. You might think the next AI coding company will be out of business in the next few years, but when these companies raise a round every 6 months doubling their valuation each time, you’re probably better off investing in them anyway.

I know, public markets are liquid so you can get out fast when everything starts collapsing, while you can’t do the same with startups.

But “markets can remain irrational longer than you can remain solvent” or, in VC words, your bet can stay contrarian longer than the company’s runway. And in a bubble market like the one described above, contrarian bets are crazy scary.

Can you really blame early-stage VC for playing the game?