Europe, it's time to build

#19 | On how to secure a brighter future for our children

In Italian we say “Non tutto il male vien per nuocere”, which roughly translates into “Not all bad things come to harm”.

Trump is bad, but maybe we can take some good out of it?

I think we can. Europe, it’s your time to shine!

My long-haired companion Chris edited this piece by rolling back the clock almost three decades to the explosive and psychedelic big beat of “Dig Your Own Hole”.

Each time I read a piece by Ben Thompson, I wonder why he’s not more famous than other well-known bloggers (in my bubble).

I’ve spent much time recently reading about China, clicking on every single link in Kyle Chan’s pieces and falling into a very deep rabbit hole. Most of Kyle’s work is about how China managed to become the global manufacturing powerhouse that it is today, and how Western countries enabled that.

What I could not understand was what it implied for the US and Europe today, and how the implications would influence industrial policies over the next few years.

Then, I stumbled across this piece that Ben Thompson wrote shortly after the 2024 US election. Reading “A Chance to Build” made things click.

The fact is that we didn’t get where we are today by chance - the current situation is one that we designed on purpose. For a long time, because of globalization, the West didn’t need more industrial output.

A problem of atom-based products is that they have non-zero marginal costs: producing things has a cost, like the materials used and labor. For every additional thing you sell, the cost to produce it doesn’t materially improve. Software is different, and that’s why it scales so well - you apply some brainpower, but the cost to produce it doesn’t change with how many licenses you sell. As the world started to open up, companies in the West realized that people in the East were willing to work for less, and offshored any process that required a lot of work and little intellectual property - Fairchild Semiconductors opened their first semiconductor assembly facility in Hong Kong, where wages were $0.25 /hour, in 1964.

Previously, hardware had been the most valuable product while software was seen as a commodity. Once the intellectual property rents of software had been separated from the capital costs of hardware, however, it was inevitable that software companies would trade at higher valuations, attract more investment, and come to dominate the U.S. technology industry, while hardware companies withered. The advent of the internet dramatically accelerated these trends, enabling further separation of software from hardware via the cloud.

https://americanaffairsjournal.org/2021/08/the-value-of-nothing-capital-versus-growth/

When we look at the value chain of many technological products today, we see the same pattern: iPhones are designed in Cupertino but assembled in China, Nvidia’s GPU are designed in Santa Clara but taped out in Taiwan, more than half Teslas sold in the world are designed in Austin but assembled in China, same goes for many other products.

This approach worked really well both for companies and consumers. Businesses have leveraged all the value created by software to grow their stock value, meanwhile customers live in a service and intellectual property economy with higher wages and better working conditions.

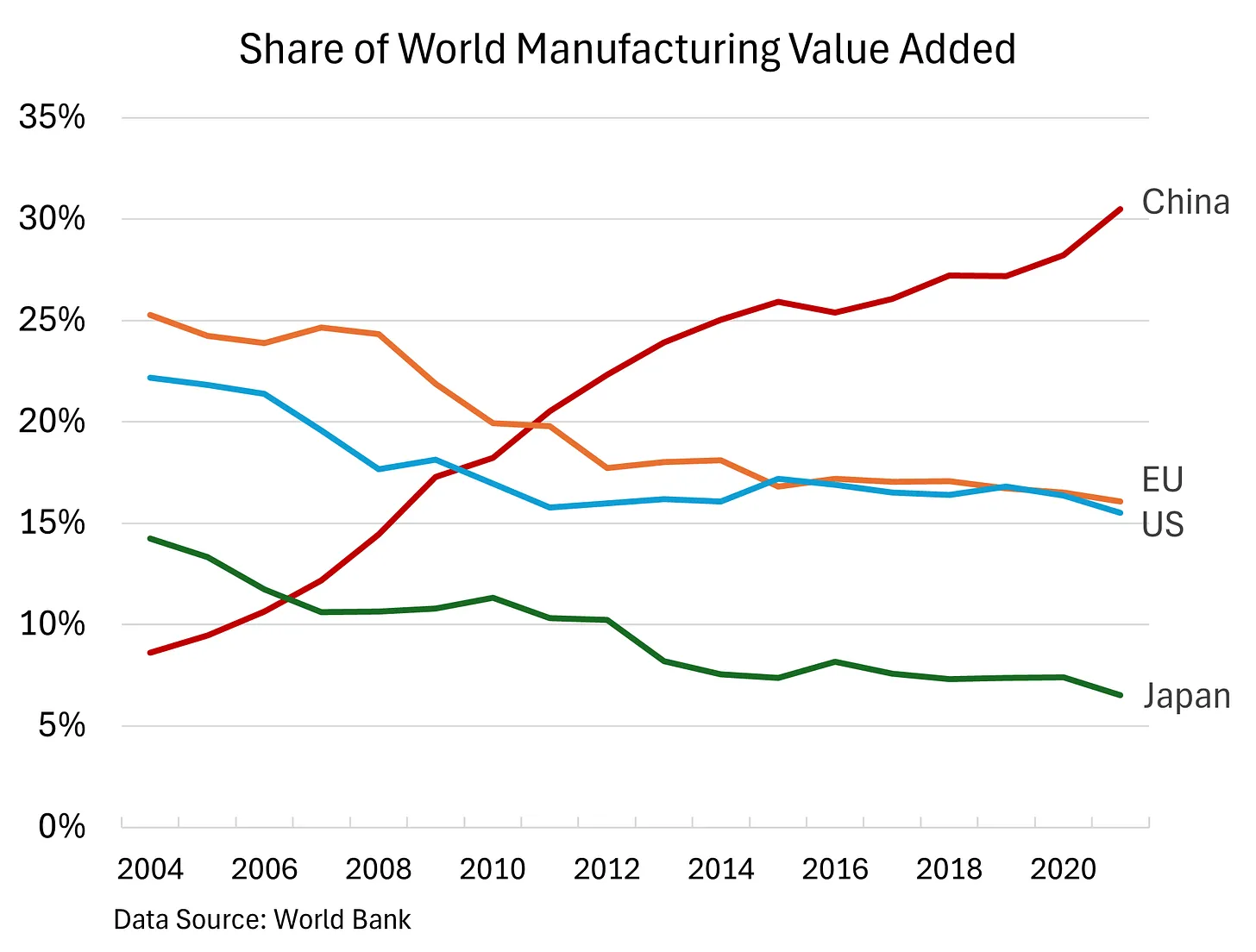

Our economies just didn’t need more industrial output, and the result is clear in the graphs below: in the last 20 years West’s share of manufacturing value added has constantly declined in favour of China, as well as the energy generated.

To many, this looked like a bargain.

We could finally stop working in factories, and start working in offices. “Building” moved from meaning turning raw material into objects to meaning turning source code into executable programs.

The problem is that, as Kyle Chan puts it, this is a Faustian bargain, and now we are starting to see the effects of it.

It’s way easier to start with labour intensive and IP-light products before moving upstream in the value chain, than it is to do the opposite. This is exactly what China did.

China never lacked hands or brains, it lacked know-how, and built a strong strategy to acquire it.

How this happened is outside of the scope of this post, and very far from being my expertise - let’s just say it has a lot to do with a very articulated industrial policy, heavy investments in commodities, short-sighted strategies from European/American companies, far-sighted strategies from Chinese companies, and technology spillover.

Now here’s the issue: as we’ve said before, it’s easier to move up the value chain once you control the bottom of it than it is to move back down the value chain once all you have is know-how.

China now dominates the production of most commodities needed to build basic hardware on which Western software should run. Moreover, there are plenty of skillful hands that know how to turn these materials into hardware, something which Europe has been gradually losing.

Jobs went on to urge that a way be found to train more American engineers. Apple had 700,000 factory workers employed in China, he said, and that was because it needed 30,000 engineers on-site to support those workers. “You can’t find that many in America to hire,” he said.

“Steve Jobs” by Walter Isaacson

Now China has a unique opportunity that it has created with its own hands and is working hard not to screw up: moving up the value chain while controlling the foundations of it.

The West has slowly moved up the value chain, offshoring large volume, low value added parts of the process to focus on highly specialized, low volume and high value added ones. Now that China is threatening the apical position with its products, it’s very painful to turn back and reconquer the foundational blocks.

When Mr. Melo bought Caldwell in 2002, it was capable of the high-volume production Apple needed. But demand for that had dried up as manufacturing moved to China. He said he had replaced the old stamping presses that could mass-produce screws with machines designed for more precise, specialized jobs. Mr. Melo thought it was ironic that Apple, a leader in offshore manufacturing, had come calling with a big order. “It’s hard to invest for that in the U.S. because that stuff is purchased very cheaply overseas,” he said.

https://www.nytimes.com/2019/01/28/technology/iphones-apple-china-made.html

On the other hand, once those owning the know-how at the top of the value chain need your products desperately, you can force them to trade them for some of their know-how. This has enabled China to move up in the value chain and slowly replace Western products with their products.

This is the story of Apple up-skilling their suppliers, that in turn start supplying local brands that end up competing with Apple’s products. This is the story of Tesla, that has taught Chinese brands how to build highly automated, vertically integrated factories, only to see the very same Chinese brands replace Tesla in markets like Europe. This is the story of Alstom and Siemens, that first exported the designs of their trains to China, and then were forced to merge to withstand the competition of the very same Chinese companies they helped emerge.

So what happens when borders close instead of opening, tariffs are imposed instead of being removed? For a long time software was the name of the game, because we took hardware for granted. We packed our homes, phones and cars with software because we never doubted we would have enough hardware or energy to run it. Now that the Pax Americana seems to be over, we are moving towards a world in which the most important technologies are made of atoms, not bits - and we need to relearn how to turn atoms into objects if we want to stay relevant.

This trend applies to the West as a whole, but more so to Europe, as we became particularly vulnerable on the topic.

First, Europe is extremely globalized.

This failure to lower internal barriers has also contributed to Europe’s unusually high trade openness. Since 1999, trade as a share of GDP has risen from 31 per cent to 55 per cent in the eurozone, whereas in China it rose from 34 per cent to 37 per cent and in the US from 23 per cent to just 25 per cent. This openness was an asset in a globalising world. But now it has become a vulnerability.

This means that we have double to lose because not only does trade make up a good part of our companies’ revenues, but also we rely on trade for a good part of our needs.

The solution to this is as easy in theory as it is hard in practice: remove the internal barriers and make trading among European countries much cheaper than it is to trade with the rest of the world.

Second, Europe is not energy independent.

The US has extensive shale oil and gas reserves, which had been inaccessible until recently, but the shale oil revolution radically changed the global energy landscape from 2010. US production of both natural gas and crude oil has more than doubled in just over a decade, providing abundant and cheap energy, and turning the US into a net energy exporter. In 2010, the US had a trade deficit in energy worth $360 billion, which by 2022 had turned into a surplus of $65 billion.

https://www.cer.eu/insights/why-europe-should-not-worry-about-us-out-performance

It is pointless dedicating any words on acknowledging the problem of being unable to produce enough of our own energy. As Dealroom puts it in his latest report Accelerating Europe: “Shale boom gave the US economy a $0.5 trillion boost, plus a strategic advantage.”

It is of utmost importance that we roll our sleeves and we diversify our energy mix, using all the resources we have (yes, nuclear, I’m looking at you) and investing in companies innovating in the energy sector - otherwise we will never be competitive again.

Third, European population is aging and declining.

There is little tech and venture capital can do to revert this trend. What can be done is, however, empower the few workers left with tools to become more productive.

Europe has lost control of many commodities that are needed to build things: we don’t produce silicon wafers, we produce little steel and aluminum, and same for many other commodities. The only way to get back into the game is to innovate on the cost side, for example finding more energy-efficient processes as energy is the main cost driver in many cases.

We also lost the ability to produce things efficiently at high volumes. We often see ourselves as artisans, but artisans don’t scale: we need automation and we need optimization, as soon as possible. Long live the artisans crafting shoes, but let’s use robots to build cars.

As Ben Thompson concluded in his piece: “It’s Time to Build.”

Geopolitical turmoil is dangerous but creates opportunities - if there is a moment to disrupt otherwise slow moving industries, that moment is now.

The real opportunity is taking advantage of robotics and AI to make physical goods into zero marginal cost items in their own right (outside of commodities; this is what has happened to chips: assembly and testing are fully automated, which makes a U.S. buildout viable).

I’m excited to see momentum picking up in Europe, companies building in the right spaces and funds investing in the right companies.

When we stop idolising the US as the prom queen, when we motivate young engineers to be excited about the built world, when we treat our neighboring European countries as partners and not competitors, only then will we be able to seriously tackle the fundamentals problems that threaten the very future of our democracies.

C’mon Europe, it’s time to build!

great work!! as always :) btw i also just published about kyle chan's amazing deep dive on china, crazy synchronicity